The Dow continues to break through to record highs, and the U.S. public equity market heads into the ninth year of a bull market—its longest ever. Looking for ways to achieve differentiated returns, investors have turned to the private market, resulting in changing dynamics in the landscape. In 2016, venture capital (VC) and private equity (PE) funds raised record levels of capital, and in 2017, investors have pushed this bullish trend upward.

Spillover dynamics from the public market into the private market have driven changes to how investment managers approach portfolio management. We identify five trends and analyze their impact on the way PE and VC investors are reacting.

1. Record High Assets Under Management (AUM)

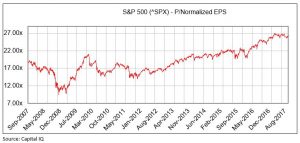

The S&P 500 has seen price to earnings (P/E) ratios creep up to their highest levels in almost 15 years. Long-term investors, with an eye for trends and a goal to find the best return on investment, have begun to allocate more capital to the private market. Seeking superior returns, these investors have flooded private industry, pushing the assets under management to more than $440 billion in VC and $1.4 trillion in PE.

2. Record-Level Dry Powder

The flood of capital into the private market has pushed the median VC fund size from $28M in 2012 to $84M today. This has put pressure on VC and PE investment managers to find opportunities that will generate adequate returns and has driven average late-stage VC deals higher to $27M, as the largest funds now invest more heavily in even later-stage companies.

Dry powder in PE has been pushed to record levels ($739 billion as of 12/31/16), as general partners are tasked with putting money to work. This solid backlog of funding will provide future support for deal flow and keep valuations high.

3. Elevated Valuations

VC investors, seeking growth, have invested larger rounds in later-stage companies, forcing the valuations of these companies like Uber and Snap (recently public), which can still be cash-flow negative, to levels that imply sustained superior growth rates. These growth projections have proven to be aggressive, however, and unsustainable. Recent revaluations of funds invested in some of these companies have proven it’s likely impossible for some of these companies to grow at rates fast enough to justify their valuations.

PE EV/EBITDA buyout multiples in 2017 have come slightly down from their 2016 records. With high multiples, PE funds are finding it more challenging to generate returns through traditional buy-out investment theses. Instead, investors are looking at smaller to middle market companies for lower entry multiples. Going down market allows fund managers to invest in smaller deals that have more reasonable valuations.

4. Active Investment Management

4. Active Investment Management

Large VC fund managers, with a trend of investing in later-stage companies, have taken more board control and recently have played a more active role in the strategy and operations of growth companies. Look no further than the world’s most valuable startup, Uber, to see how fund managers have started to flex their muscles.

When buying smaller companies, investors must operate them more aggressively—improvements take longer, and it’s a longer road to return on invested capital. PE firms, seeking to differentiate themselves in a crowded industry, have refined investment theses to a greater focus on unique operational improvements. These operational improvements bring with them a need for a more intensive, tactical management strategy that pushes the PE industry from its more traditional financial role to a role focused on developing and managing operations of sound companies.

5. A Unique Exit Environment

Aggressive growth projections of late-stage startups have investors seeking to reconcile private valuations based on frothy assumptions with a public market view more focused on fundamentals. Many of these “unicorns”, especially those that continue to burn cash, will face a crunch in deciding when to accept a potential down-round into an initial public offering to obtain cash necessary to fuel growth. Late-stage investors who invested at higher valuations will be the last holdouts on the path to fundraising in the public markets.

PE investors, acquiring companies at high valuations, have also started to hold investments longer to realize the returns from implementing operational improvements. Alignment of strategy and operational goals with those of industry leaders could prove beneficial for PE investors when seeking exits through strategic sales.

As we watch the bull market continue higher and fund managers are forced to put capital in play, the private market will prove interesting to watch as VC and PE funds evolve to meet the demands of their investors.

For more information about how MorganFranklin can assist your organization, visit our Private Equity services page.